Reports in the 'Company' Area

Last updated on 2026-05-15

Overview

Four different reports are available in the Company area. This chapter describes the purpose for which the reports can be used.

This article contains the following sections:

Navigation

The reports can be found under Company | Deferred Taxes | Reports.

The Report DT is displayed, for example, as follows:

Available Reports

The following reports are available:

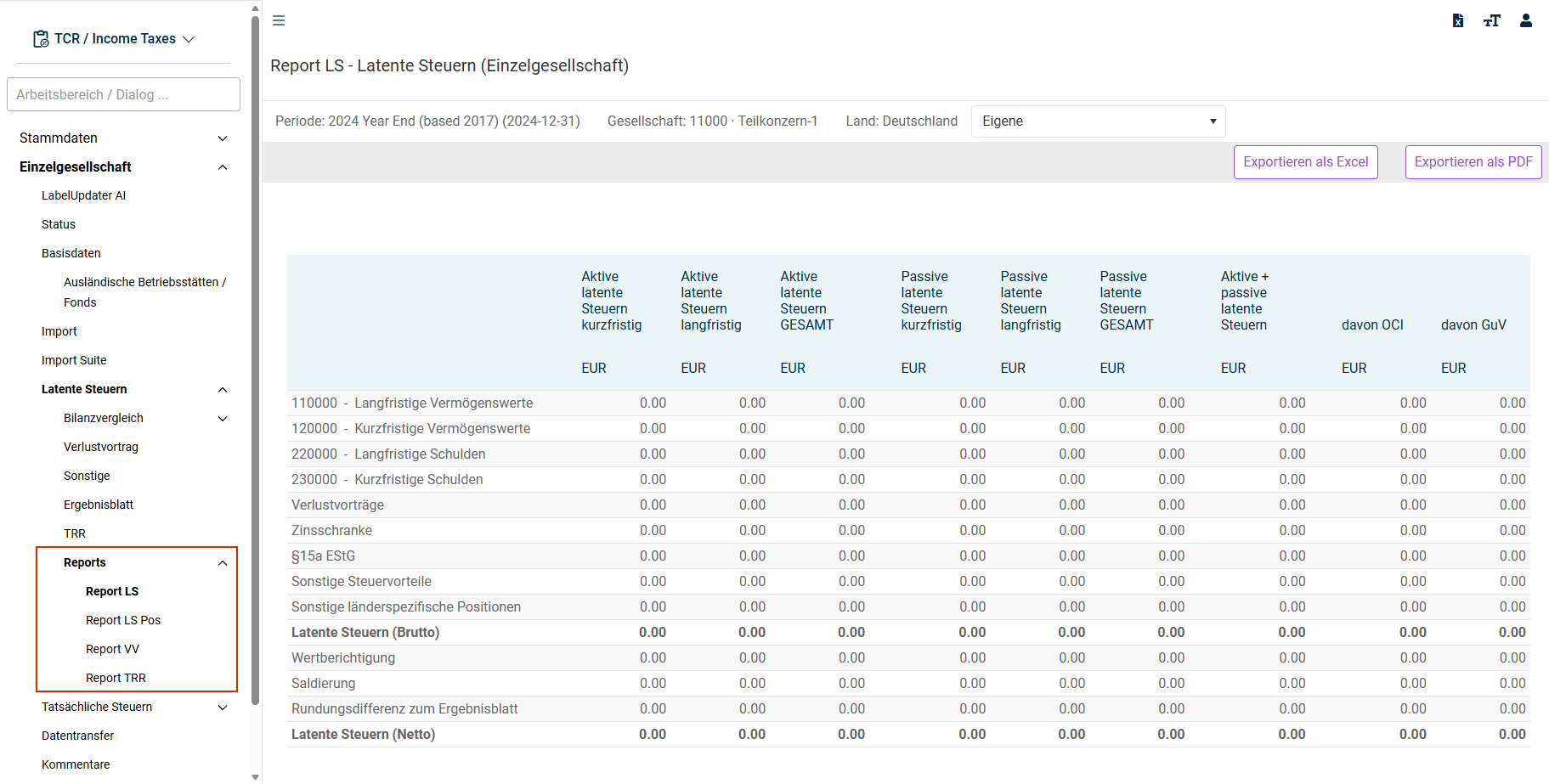

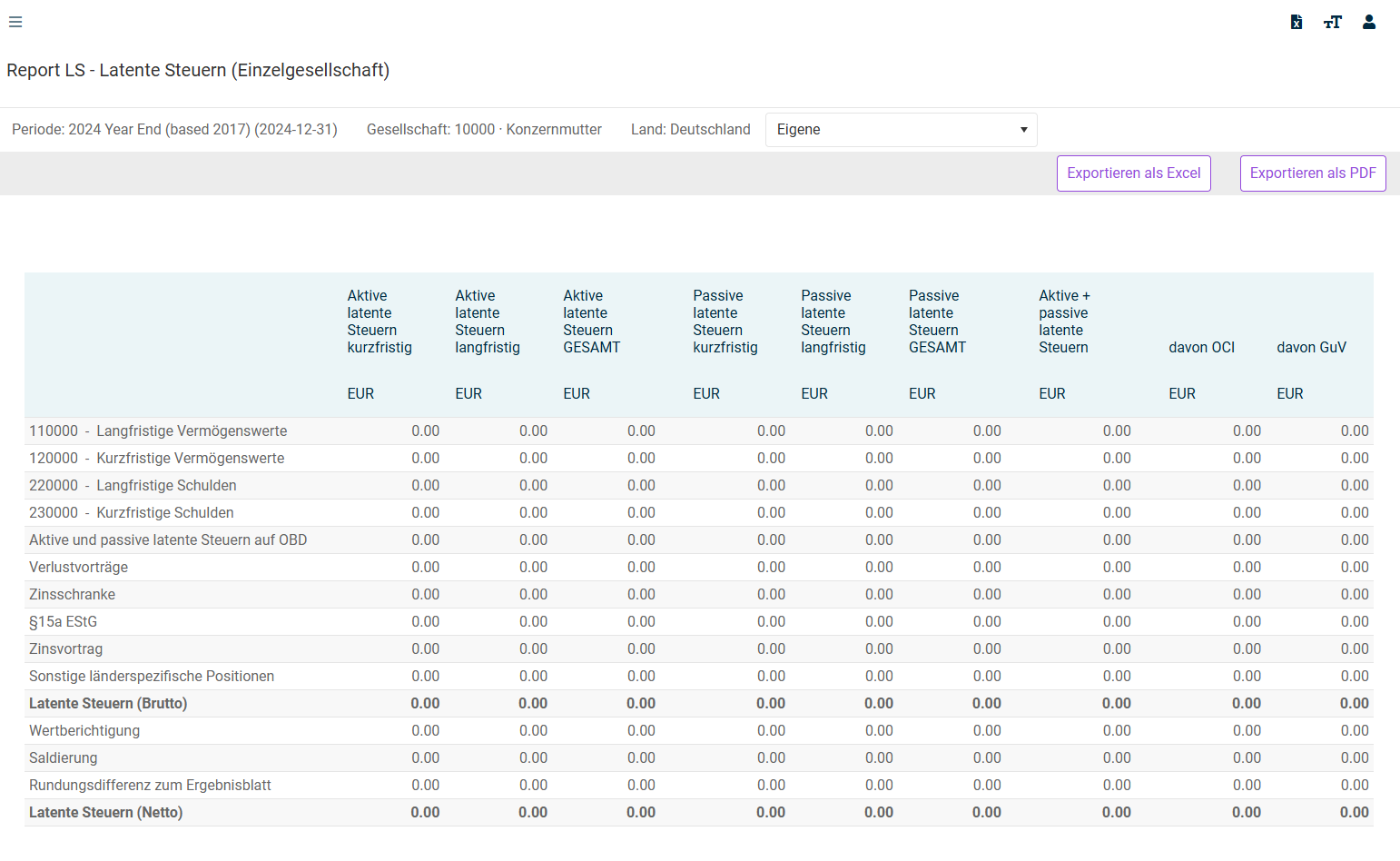

Report DT

The Report DT aggregates the deferred taxes calculated in the B/S Comparison and LCF (Loss carried forward) workspaces. In addition, the deferred taxes entered in the Others workspace are also taken into account. The Report DT differentiates the maturity of the individual balance sheet items and can be used as a disclosure in accordance with IAS 1.61 / 12.81g.

The Report DT is displayed as follows:

The structure of the condensed balance sheet in the Report DT is based on the settings in the CoA Group master data dialog. Only (parent) items for which the Disclosed major class of deferred tax attribute is activated are displayed in the Report DT. An incorrect configuration may result in a discrepancy between the deferred taxes displayed in the Report DT and those in the Summary.

All sub-workspaces are used for the deferred taxes from the balance sheet comparison (including, for example, any supplementary balance sheets that may exist). The Other Country Specific Positions row is derived from the Others workspace. The same applies to the Unrecognised DTA (after re-assessment) row.

A validation is performed in the bottom row of the workspace. The values must equal zero.

The Report DT does not include any deferred taxes acquired through additions, e. g. in the case of tax groups. Only the deferred taxes of the chosen company are displayed.

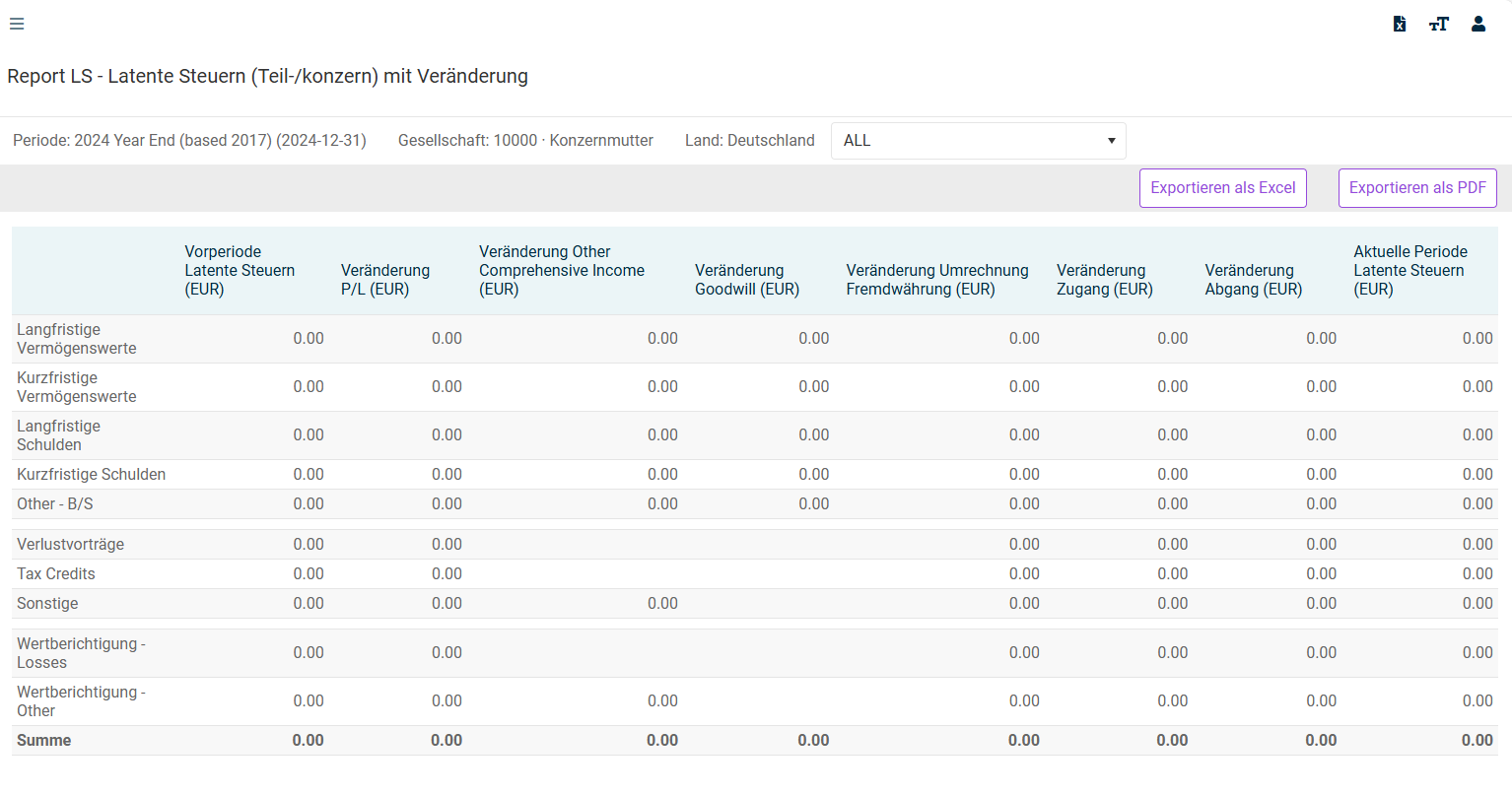

Report DT Pos

The Report DT Pos in the (Sub-)Group area aggregates the total change in deferred taxes of the subordinate or dependent individual companies for each balance sheet item. This involves a rollforward calculation of the deferred taxes from the previous period to the current period.

The Report DT Pos is displayed as follows:

The structure of the (condensed) balance sheet in the Report DT Pos is based on the settings in the CoA Group master data dialog. Only (parent) items for which the Disclosed major class of deferred tax attribute is activated are displayed in the Report DT Pos.

In the header row, the view can be switched between ALL, DTA and DTL. If the DTA option is selected, only the deferred tax assets, for example, are displayed – any deferred tax liabilities are hidden.

The Total row can also be reconciled with the Deferred Taxes workspace in the (Sub-)Group function area. The explanations made there therefore apply when determining the individual change columns.

In addition to this condensed overview, there is also a very detailed technical report that shows the underlying values for each company. You can find this under Reporting | Tax Reports under Deferred taxes per position with change (data IDs). Based on this report, you can create a custom report in the required structure.

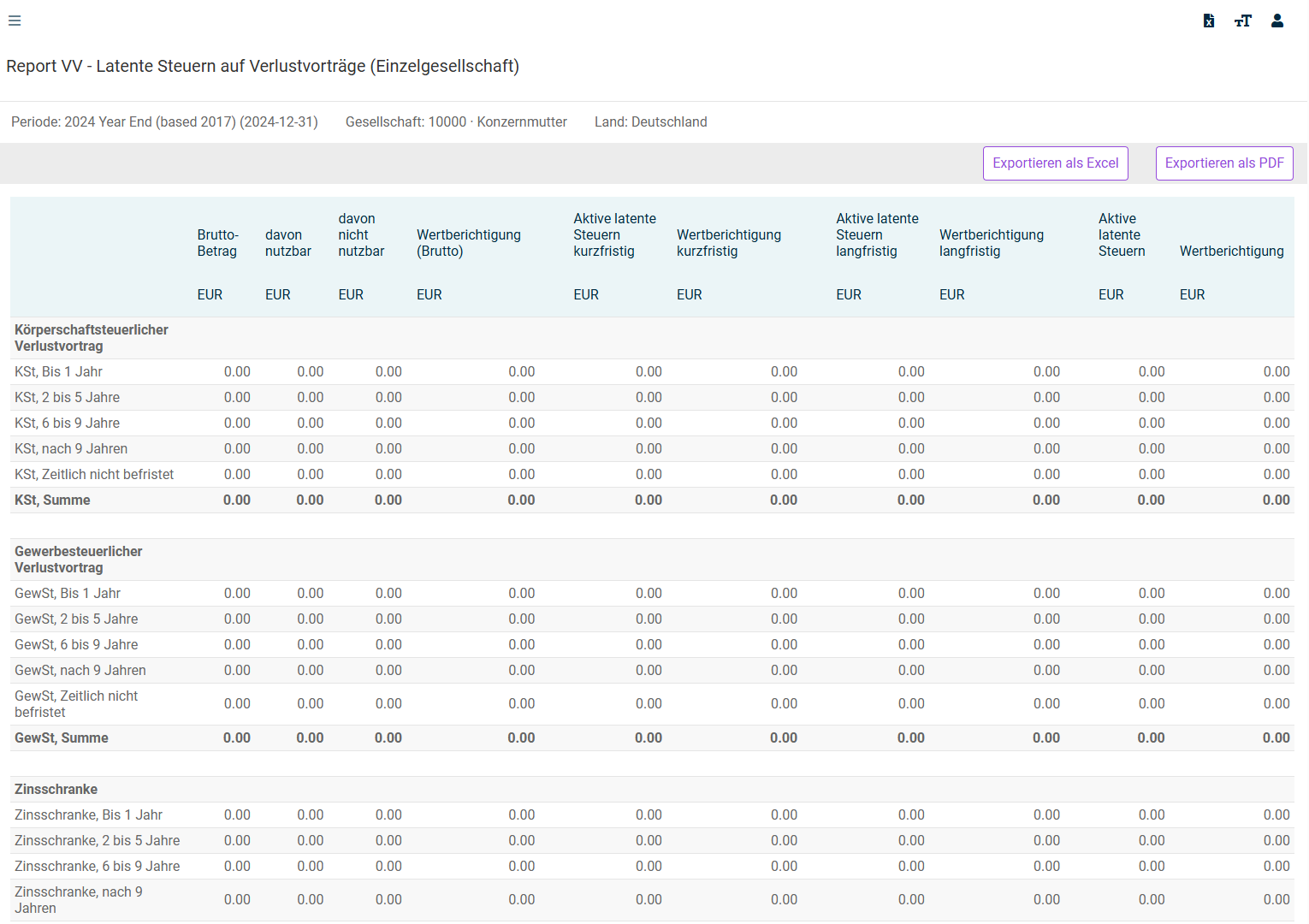

Report DT (LCF)

The Report DT (LCF) aggregates the deferred taxes calculated in the LCF workspace and provides an overview of the balances. The report can be used, among other things, as a disclosure in accordance with IAS 12.81e. In addition, allowances for deferred tax assets from losses carried forward are also displayed [IAS 12.80g].

The Report DT (LCF) is displayed as follows:

The Report DT (LCF) can be reconciled with the summary.

The Report DT (LCF) does not include any deferred taxes acquired through additions, e. g. in the case of tax groups. Only the deferred taxes of the chosen company are displayed.

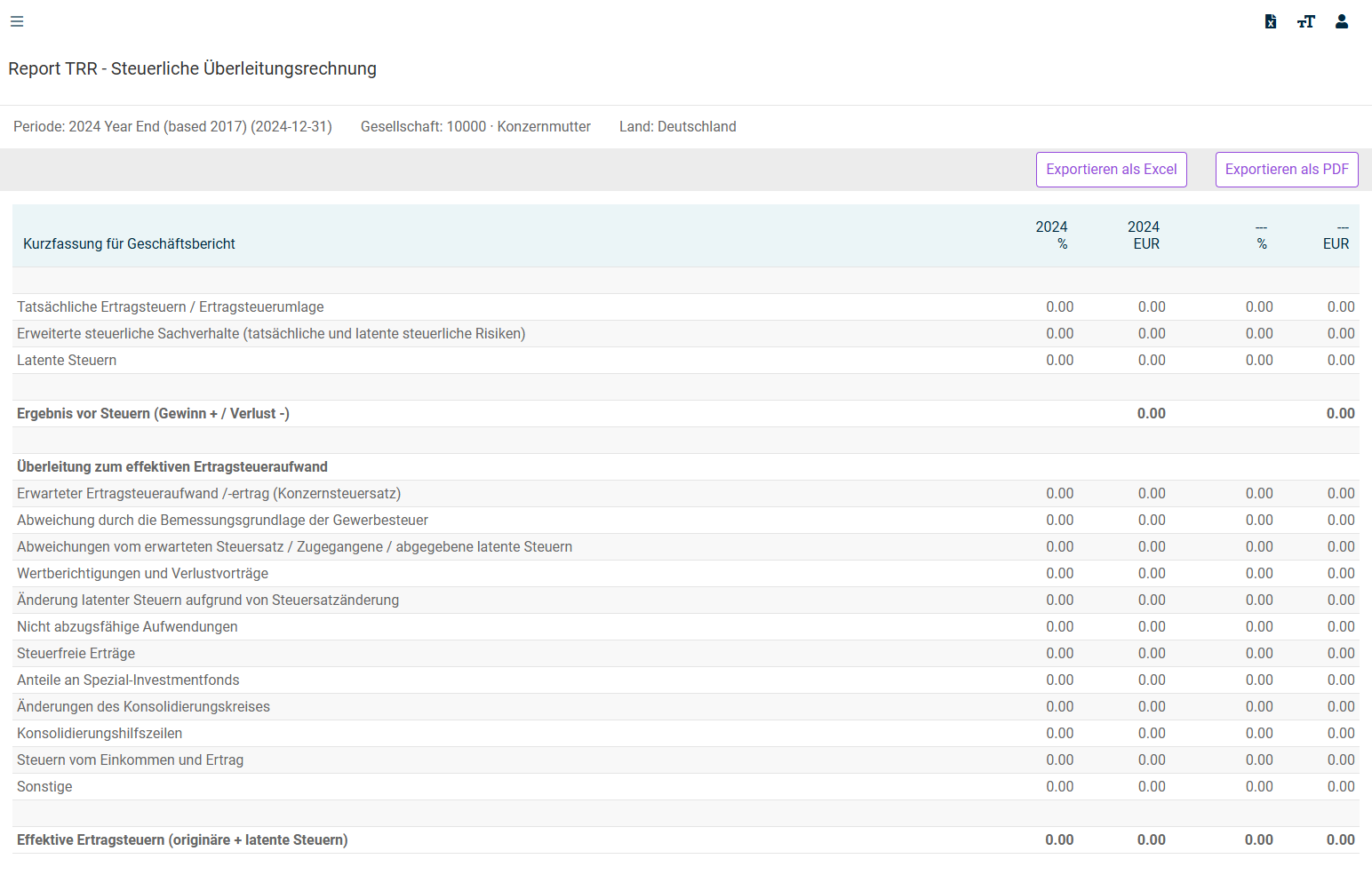

Report TRR

The Report TRR aggregates the report from the TRR workspace at group level in the form of a summary for the annual report. The report can be used as a disclosure in accordance with IAS 12.81c — the standard setter does not prescribe a fixed structure for the tax rate reconciliation.

The Report TRR is displayed as follows:

The Report TRR contains the following two permitted presentation formats:

A reconciliation between the tax expense (tax income) and the expected income tax expense [IAS 12.81c i]

A reconciliation between the average effective tax rate and the applicable tax rate [IAS 12.81c ii]