FTE & PE Allocations

Last updated on 2026-01-23

Overview

In the FTE & PE Allocations workspace, you can manage cross-border allocations of income or loss and taxes between a parent entity and its permanent establishment (PE) or a flow-through entity (FTE). The interface enables you to view both Outgoing allocations and Incoming allocations, providing flexibility in managing financial movements. It also supports supports adjustment types for Substance-Based Income Exclusion (SBIE) allocations as well as exporting allocation data as an Excel or pdf file for reporting and analysis. Additionally, the Pillar 2 module includes filtering and search functionalities to manage and organize data efficiently.

Note: The effect an allocation has on the CE calculations depends on the adjustment type:

- Financial accounting net income or loss adjustments are considered in INC-1.2 and INC-1.3.

- Current taxes adjustments are considered in CT-1.2 and CT-1.3.

- Payroll Costs (SBIE) adjustments are considered in CO-1A and affect CO-1.

- Tangible Assets (SBIE) adjustments are considered in CO-2A and affect CO-2.

This article contains the following sections:

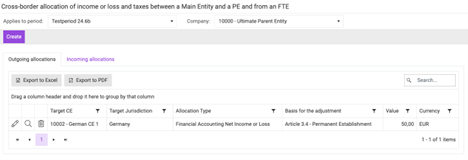

Navigation

The FTE & PE Allocations workspace can be found at Pillar 2 | Entity Data Collection | FTE & PE Allocations. The workspace is displayed as follows, for example:

'FTE & PE Allocations' workspace

'FTE & PE Allocations' workspace

Note: The effect an allocation has on the CE calculations depends on the adjustment type:

- Financial accounting net income or loss adjustments are considered in fields INC-1.2 and INC-1.3.

- Current taxes adjustments are considered in fields CT-1.2 and CT-1.3.

Creating New Allocations

In addition to importing allocations, you also have the option to manually create new allocations. To create a new FTE or PE allocation:

- Select a period from the Applies to period drop-down menu.

- Select the source CE from the Company drop-down menu.

- Click Create.

- Select the following:

- Target CE

- An adjustment type:

- Financial accounting net income or loss

- Current taxes (FTE or PE)

- Payroll costs

- Tangible assets

- Select the legal basis for the adjustment:

- For a financial accounting income or loss adjustment:

- Article 3.4 - Permanent establishment;

- Article 3.5.3 - Other owners that are not group entities (flow-through);

- Article 3.5.1 (a) - Permanent Establishment (flow-through);

- Article 3.5.1 (b) CE-owner (flow-through).

- For a current taxes (FTE or PE) adjustment:

- Article 4.3.2 (a) - Permanent Establishment;

- Article 4.3.2 (b) - Tax transparent entity;

- Article 4.3.2 (d) - Hybrid entity;

- Article 4.3.4 - Loss making permanent establishment.

- For a payroll cost adjustment:

- SBIE to PE - Addition to the Eligible Payroll Costs of the PE;

- SBIE from FTE - Addition to the Eligible Payroll Costs of the CE-Owner.

- For a tangible asset adjustment:

- SBIE to PE - Addition to the Carrying value of relevant Eligible Tangible Assets of the PE;

- SBIE from FTE - Addition to the Carrying value of relevant Eligible Tangible Assets of the CE-Owner.

- For a financial accounting income or loss adjustment:

- Enter the amount:

- For income/loss or current taxes adjustments: Enter the amount for the addition to the covered taxes of the other constituent entity in the local currency of the source CE.

- For payroll cost adjustments: Enter the payroll cost amount to allocate in the local currency of the source CE.

- For tangible asset adjustments: Enter the tangible asset value to allocate in the local currency of the source CE.

- Click Save.

Editing Existing Allocations

To edit an existing tax allocation:

- Select a period from the Applies to period dropdown menu.

- Select the source CE from the Company dropdown menu.

- Click the edit button (the little pencil) next to the allocation.

- Select an adjustment type:

- Financial accounting net income or loss;

- Current taxes (FTE or PE);

- Payroll costs;

- Tangible assets.

- Select the legal basis for the adjustment:

- For a financial accounting income or loss adjustment:

- Article 3.4 - Permanent establishment;

- Article 3.5.3 - Other owners that are not group entities (flow-through);

- Article 3.5.1 (a) - Permanent Establishment (flow-through);

- Article 3.5.1 (b) CE-owner (flow-through).

- For a current taxes (FTE or PE) adjustment:

- Article 4.3.2 (a) - Permanent Establishment;

- Article 4.3.2 (b) - Tax transparent entity;

- Article 4.3.2 (d) - Hybrid entity;

- Article 4.3.4 - Loss making permanent establishment.

- For a payroll cost adjustment:

- SBIE to PE - Addition to the Eligible Payroll Costs of the PE;

- SBIE from FTE - Addition to the Eligible Payroll Costs of the CE-Owner.

- For a tangible asset adjustment:

- SBIE to PE - Addition to the Carrying value of relevant Eligible Tangible Assets of the PE;

- SBIE from FTE - Addition to the Carrying value of relevant Eligible Tangible Assets of the CE-Owner.

- For a financial accounting income or loss adjustment:

- Enter the amount:

- For income/loss or current taxes adjustments: Enter the amount for the addition to the covered taxes of the other constituent entity in the local currency of the source CE.

- For payroll cost adjustments: Enter the payroll cost amount to allocate in the local currency of the source CE.

- For tangible asset adjustments: Enter the tangible asset value to allocate in the local currency of the source CE.

- Click Save.

Notes:

- Optionally, you can upload supporting documents as an attachment to the allocation or add a description, e.g. a comment that explains divergences from prior years.

- Allocations use the local currency of the source CE.

- The Incoming allocations tab is purely informational. Entering new allocations or editing existing allocations must be done outgoing from the source CE.

Notes on SBIE Allocations

The Payroll Costs and Tangible Assets adjustment types are used specifically for Substance-Based Income Exclusion (SBIE) calculations. These allocations allow you to properly attribute SBIE substance factors between constituent entities in complex structures involving permanent establishments and flow-through entities.

Use Payroll Costs allocations when:

- Employees are formally employed by one constituent entity but perform work that should be attributed to another entity (typically a permanent establishment)

- A flow-through entity has payroll costs that should be attributed to the CE-Owner for SBIE purposes

- You need to adjust eligible payroll costs for SBIE calculation compliance

Use Tangible Assets allocations when:

- Tangible assets are owned by one constituent entity but used by another consitutent entity (typically a permanent establishment)

- A flow-through entity owns tangible assets that should be attributed to the CE-Owner for SBIE purposes

- You need to adjust the carrying value of eligible tangible assets for SBIE calculation compliance