OECD-Standard

Last updated on 2026-04-14

Overview

The Pillar 2 module closely follows OECD model rules and the GloBE Information Return (GIR). Therefore, the OECD-Standard folder and its workspaces include all data points and entity-level elections required by the OECD and nothing else.

- Certain elections can result in some of the values in this folder being omitted from the calculations.

- Users can assess the impact of an election by first entering all entity data and then creating one snapshot with and one without applying that election.

- Values for constituent entities that have excluded entity status or that are not a constituent entity for Pillar 2 purposes are set to 0 in the CE calculations and the jurisdictional blending.

The field EE-4 in the Entity Election and General Information workspace removes the excluded entity status.

This article contains the following sections:

Navigation

The OECD-Standard folder and its workspace can be found under Pillar 2 | Entity Data Collection and is displayed as follows, for example:

Description of OECD-Standard Workspaces

The OECD-Standard folder contains the following workspaces:

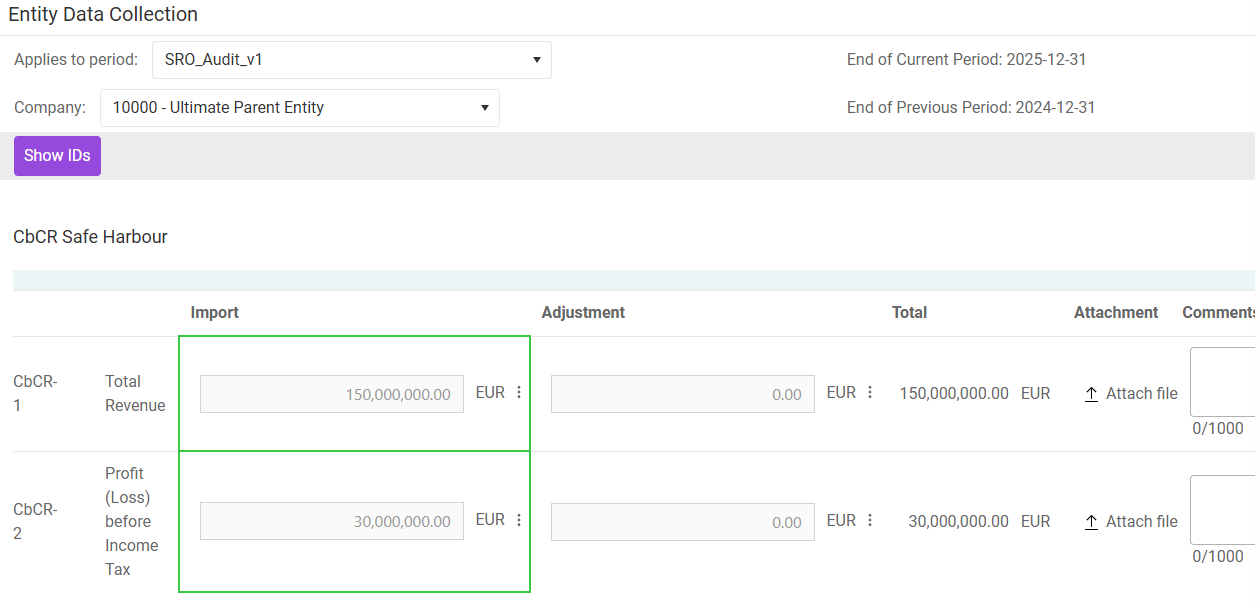

This workspace stores information relevant to the simplified ETR test and the de minimis exclusion that are part of the transitional safe harbour rules. The entries in this workspace must be in accordance with the corresponding entries in the CE’s country-by-country report. Hence, Lucanet highly recommends that users who also use the CbCR module import CbCR safe harbour data from there.

This workspace stores information required for the third part of the transitional safe harbour check, the substance-based income exclusion, and to calculate the carve-out amount in the CE calculations and in the jurisdictional blending.

Notes:

The tangible asset-carve out amount is calculated as the average of the sums for the reporting year and for the preceding year. Therefore, a prior period that includes the ultimo exchange rates for all jurisdictions is required for this calculation.

If there is no prior period, or if a jurisdiction is missing from that period, a default exchange rate of 1:1 will be used. For example, a German MNE Group that reports in Euro acquires its first Austrian company in 2025. Since Austria also uses the Euro, the calculations for the reporting fiscal year 2025 will yield the same results whether Austria gets added to the period for 2024 (with an exchange rate of 1:1) or not (in which case the default rate of 1:1 will be applied).

If a user elects to apply the substance-based income exclusion, the calculations will ignore any values in this workspace. Users can base their decision for or against that election by comparing snapshots with and without it.

This workspace contains the entity-level elections and general information regarding the applicable qualified domestic top-up tax (QDMTT) and accounting standard:

Simplified jurisdictional reporting framework

EE-1 allows the MNE Group to elect a simplified reporting approach during the transitional period. This field is marked as informational only, i.e. this is an informational election that helps document the group's approach to jurisdictional reporting. Activating this checkbox documents the election but does not directly affect calculations.

Annual Elections

Annual elections only apply to the current reporting period and can be made differently for every year. The Annual Elections section provides the following:

EE-2 Debt Release Election (Article 3.2.1)

- EE-2 controls whether debt release income is included in the CE calculation and jurisdictional blending.

- Activate this checkbox to include values stored at INC-2.11 in C2 - CE Calculations and in C4- Jurisdictional Blending. Otherwise, those values will be disregarded, and the debt release income will not affect the constituent entity's GloBE income.

EE-3 Unclaimed Accrual Election (Article 4.4.7)

- EE-3 addresses the treatment of unclaimed accruals in the covered taxes calculation, and relates to adjustments for amounts that were accrued but never paid.

- This field is marked as informational only , i.e. it documents the MNE Group's approach to unclaimed accruals.

Five-year Elections

Five-year elections apply for the period of five years and cannot be changed within that period. The Five-year Elections section provides the following:

EE-4: Not Treating an Entity as an Excluded Entity Election (Article 1.5.3)

- A constituent entity that meets at least one of the criteria represented by AMAE20 to AMAE26 has excluded entity status. All values relating to an excluded entity are set to 0 in the CE calculations and the jurisdictional blending.

- However, EE-4 supersedes AMAE20 to AMAE26 and removes excluded entity status. By activating the checkbox, values for the constituent entity are included in the CE calculations and jurisdictional blending, and the entity is treated as a regular constituent entity for Pillar 2 purposes.

EE-5: Inclusion of All Dividends with Respect to Portfolio Shareholdings (Article 3.2.1(b))

- EE-5 controls the treatment of dividend income from portfolio shareholdings, and allows the MNE Group to elect to include all portfolio dividends in GloBE income, even if they would otherwise be excluded.

- This field is marked as informational only, but, for documentation purposes, we recommend to activate the checkbox, if necessary.

EE-6: Treating Foreign Exchange Gains or Losses Attributable to Hedging as an Excluded Equity Gain or Loss (Article 3.2.1(c))

- EE-6 controls the treatment of foreign exchange (FX) gains and losses arising from hedging activities, anda llows such FX gains/losses to be treated as excluded equity gains or losses.

- These FX items are removed from GloBE income, similar to how equity gains/losses are treated.

- This field is marked as informational only, but consider activating if the group has significant hedging activities that create FX volatility.

EE-7: Investment Entity Tax Transparency Election (Article 7.5)

- EE-7 allows investment entities to be treated as tax transparent for Pillar 2 purposes, and changes how income and taxes of investment entities flow through to their owners.

- Activate this checkbox if you want the investment entity to be treated as tax transparent.

EE-8: Taxable Distribution Method Election (Article 7.6)

- EE-8 controls how distributions from tax-transparent entities are treated in Pillar 2 calculations, and specifically addresses the taxable distribution method for certain ownership structures.

- Activate this checkbox if you want values of the respective constituent entity that are added at INC-2.24 and CT-2.16 to be taken into account in C2 - CE calculation and C4 - Jurisdictional Blending, and if distributions subject to withholding or other taxes are to be recognized in the GloBE calculations.

- If you do not activate the checkbox, any values added at INC-2.24 and CT-2.16 are not taken into account for the respective CE.

EE-9: Simplified ETR Election for Non-Material Entities

- EE-9 allows the use of a simplified effective tax rate calculation for non-material constituent entities (NMCEs), and reduces the compliance burden for entities that have minimal impact on the overall Pillar 2 calculation.

- This field is marked as informational only, but consider activating the checkbox to document which entities qualify as non-material. When activated, NMCEs can use simplified methods to calculate their ETR.

Option

Description

NMCE Safe Harbour

NMCE Safe Harbour settings provide a simplified compliance option for Non-Material Constituent Entities (NMCEs).

EE-1

Simplified Calculation for NMCEs

Activate this checkbox if your CE qualifies for the NMCE Safe Harbour, i.e. C2 – CE Calculations, C4 - Jurisdictional Blending, and C5 – Top-up Tax Allocation are excluded from the Pillar 2 calculations (see also C1 – NMCE Safe Harbour).

Annual Elections

Annual elections only apply to the current reporting period and can be made differently for every year.

EE-2

Debt Release election (Article 3.2.1)

Activate this checkbox to include values stored at INC-2.11 in the CE calculation (C2) and in the jurisdictional blending (C4). Otherwise, those values will be disregarded.

Five-year Elections

Five-year elections apply for the period of five years and cannot be changed within that period.

EE-4

Not treating an Entity as an Excluded Entity election (Article 1.5.3)

A constituent entity that meets at least one of the criteria represented by AMAE20 to AMAE26 has excluded entity status. All values relating to an excluded entity are set to 0 in the CE calculations and the jurisdictional blending. However, EE-4 supersedes AMAE20 to AMAE26 and removes excluded entity status. Consequently, by activating the checkbox for EE-4, you can include in the CE calculations and the jurisdictional blending values for otherwise excluded entities.

EE-8

Taxable distribution method election (Article 7.6)

If elected, values of the respective CE that are added at INC-2.24 and CT-2.16 are taken into account in the CE calculation as well as the jurisdictional blending. If not elected, any values added at INC-2.24 and CT-2.16 are not taken into account for the respective CE.

Note: EE-3, EE-5, EE-6, and EE-9 are for informational purposes only.

The data in this workspace is used to calculate the GloBE income of the CEs (C2 – CE-Calculations) and in the several jurisdictions (C4 – Jurisdictional Blending).

The data in this workspace is used to calculate the GloBE income of the CEs (C2 – CE-Calculations) and in the several jurisdictions (C4 – Jurisdictional Blending).

The data in this workspace is used to calculate the GloBE income of the CEs (C2 – CE-Calculations) and in the several jurisdictions (C4 – Jurisdictional Blending).

Deferred Tax Expense Calculation with GloBE Carrying Values

To comply with OECD requirements, deferred tax expenses must be calculated using GloBE carrying values rather than financial accounting carrying values. For the calculation process, you need to specify the following:

DT-1.1 - Deferred tax expense in the financial accounts: This field contains the total deferred tax expense as recorded in the financial accounts. You can either import this value from financial accounting systems or enter it manually.

DT-1.2 - Deferred tax expense in relation to assets or liabilities for which the GloBE carrying value is different to the accounting carrying value: This field captures the portion of deferred tax expense that relates to assets or liabilities where the GloBE carrying value differs from the accounting carrying value. This represents the deferred tax amount that needs to be recalculated.

DT-1.3 - Deferred tax expense based on the GloBE carrying value of assets or liabilities: This field contains the recalculated deferred tax expense using GloBE carrying values for the relevant assets or liabilities.

DT-1 - Total Deferred Tax Expense: This field is now automatically calculated using the formula: DT-1.1 - DT-1.2 + DT-1.3.

Recast Mechanism

If the entity tax rate (DT-4.1) is below the minimum tax rate of 15%, the deferred tax expense amount is recast to the minimum tax rate. If performed, the recast is crucial to the calculation of the total deferred tax adjustment amount. The recast is done by dividing the total deferred tax adjustment amount before recast (DT-3) by the entity tax rate and multiplying the result by the minimum tax rate.

Because not all deferred taxes were necessarily calculated with the same tax rate, users can define amounts A (DT-4.3) and B (DT-4.5) that will be calculated by using tax rates A (DT-4.4) and B (DT-4.6), respectively. Tax expenses must be entered as positive values in DT-4.3 or DT-4.5, tax income must be entered as negative values. The residual deferred tax expenses (DT-4.1) are calculated automatically.

The information in this workspace is used to calculate or maintain taxes on items that are excluded from the GloBE income. The structure of the workspace is as follows:

Tax Rates

The top section of the workspace contains the current tax rate and the deferred tax rate for excluded items. You have the option to manually enter the tax rates, import them, and to make manual adjustments to imported tax rates.

Taxes on Excluded Items

The entries in this section follow the same basic structure:

- The first line (e.g. EX-2.1) states the name of the GloBE adjustment and the article in the OECD model rules the exclusion is based on (e.g. Excluded Dividends - Article 3.2.1 (b)). This line contains the total value of the excluded item or items in the respective category. You have the option to upload supporting material or enter a comment of up to 1000 characters.

- The second line (e.g. EX-2.2) shows the relevant current tax expenses.

- The third line (e.g. EX-2.3) shows the relevant deferred tax expenses.

- The second and third lines each contain the following entries:

- Amount Excluded: the relevant amount excluded from the GloBE income. This value must be imported internally (from other Lucanet TCR modules) or from external sources (csv, data transfer).

- Suggestion: the suggested tax amount based on the excluded amount and the relevant tax rate.

- Adjustment Import: imported adjustments to the suggested tax amount. This value can be imported internally (from other Lucanet modules) or from external sources (csv, data transfer).

- Adjustment Manual: manual adjustments to the suggested tax amount.

- Total: the sum of the suggested tax amount and all adjustments.

Notes:

Lines EX-X.1 are for informational purposes only.

Only values in lines EX-X.2 and EX-X.3 are part of the calculations. For example, to calculate current and deferred taxes on excluded dividends pursuant to Article 3.2.1 (b) of the OECD Model Rules, you need to import or manually input the necessary data in lines EX-2.2 and EX-2.3, respectively.

Some entries only have current (e.g. EX-16.2) or deferred taxes (e.g. EX 26.3).

You can leave the Amount Excluded field empty in some or all lines and instead enter the whole tax amount as an import or manual adjustment.

Certain non-taxable transaction have no effect on current or deferred tax expenses. Thus, the amount in the first line of an entry might be different from the sum of the amounts in the other lines.

This workspace stores the inclusion ratio for the allocation of the top-up tax to individual CEs.

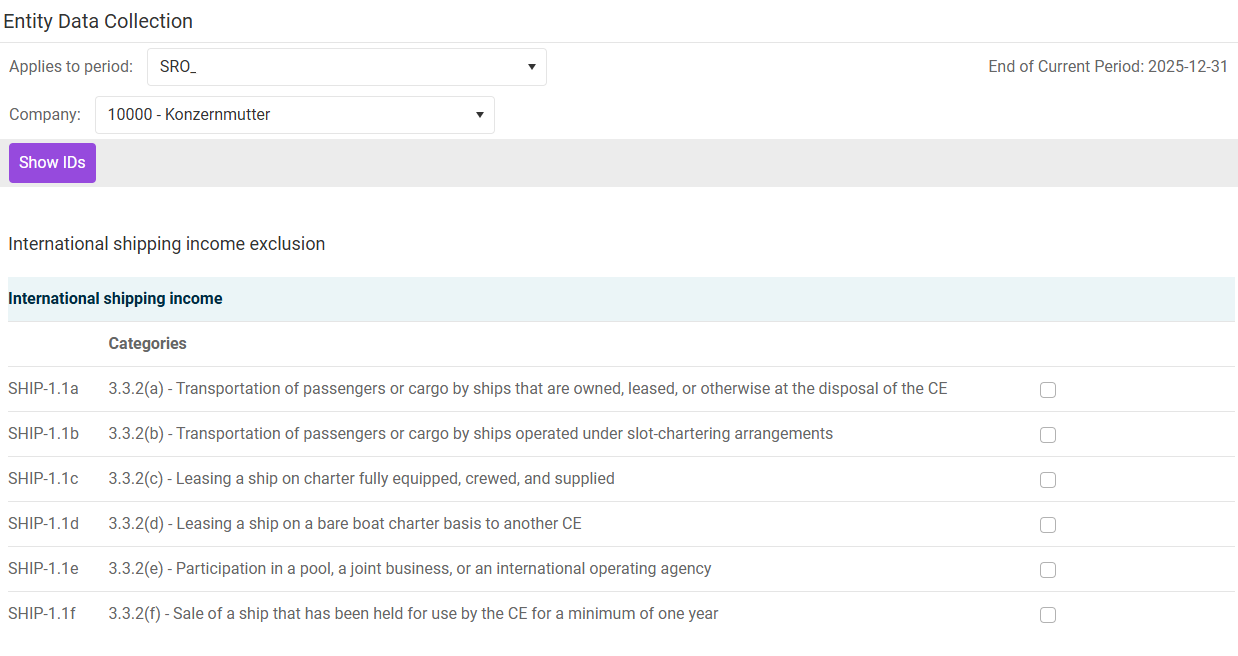

The International Shipping workspace stores data on income and expenses related to international shipping activities in accordance with Article 3.3.2 and Article 3.3.3 of the OECD Model Rules. International shipping income that qualifies under these articles can be excluded from the standard GloBE income calculation, subject to specific conditions and limitations.

'International Shipping' workspace (extract)

'International Shipping' workspace (extract)

International Shipping Income

In compliance with OECD Article 3.3.2, this section captures income from core international shipping activities. Proceed as follows:

Activate the checkbox(es) for the applicable categories in the International Shipping Income section.

Specify the total revenue from the selected international shipping activities in the SHIP-1.2 section.

Specify the costs attributable to these activities in the SHIP-1.3 section.

The International Shipping Income will automatically be calculated as the net income (revenue minus costs) and displayed in the SHIP-1 section.

Qualified Ancillary International Shipping Income

This section captures ancillary income related to international shipping operations as defined in OECD Article 3.3.3. This income is subject to a cap at the jurisdictional level.

Proceed as follows:

Activate the checkbox(es) for the applicable categories in the Qualified Ancillary International Shipping Income section.

Specify the total revenue from the selected qualified ancillary activities in the SHIP-2.2 section.

Specify the costs attributable to these activities in the SHIP-2.3 section.

The Qualified Ancillary International Shipping Income will automatically be calculated as the net income (revenue minus costs) and displayed in the SHIP-2 section.

Note: The qualified ancillary international shipping income (SHIP-2) is subject to a 50% cap relative to the total international shipping income (SHIP-1) at the jurisdictional level in C4 - Jurisdictional Blending. This cap is applied automatically during the jurisdictional aggregation process.

Effect on Substance-based Income Exclusion

Because international shipping income is excluded from GloBE income, the related payroll costs and tangible assets must also be excluded from the substance-based income exclusion (carve-out) calculations to maintain consistency.

Proceed as follows:

In SHIP-3.1, specify the payroll costs related to employees engaged in the international shipping activities. This amount will be subtracted from the eligible payroll costs used in line CO-1B in the C2 - CE Calculations workspace.

In SHIP-3.2, specify the carrying value of tangible assets (e.g., ships, equipment) used in the international shipping operations. This amount will be subtracted from the eligible tangible assets used in line CO-2B in the C2 - CE Calculations workspace.

Covered Taxes

This section is used to provide covered tax data attributable to the excluded International Shipping Income or Qualified Ancillary International Shipping Income. Enter the covered taxes related to the international shipping income that is being excluded in SHIP-4. These taxes will be subtracted from the current tax expense on excluded items in line CT-2.6 in the C2 - CE Calculations workspace.

Notes:

- Make sure to specify all values in the local currency of the CE. Currency conversion to the snapshot currency is performed automatically during snapshot creation.

- You can attach supporting documents and comments to provide additional context or justification for the values entered.

- The data from this workspace is transferred to the International Shipping Income Exclusion section of the C2 - CE Calculations workspace.

- At the jurisdictional level in the C4 - Jurisdictional Blending workspace, the ancillary income cap is applied automatically, and the combined shipping income exclusion (SHIP-1 + SHIP-2B) is reflected in line INC-2.25.