Configuring Investments

Last updated on 2025-07-02

Overview

The Investment accounting rule type can be used to plan new investments and their depreciation/amortization. The configuration specifies the bank account, value-added tax and cash flow impact. Furthermore, the rule including the useful life and the accounts for the accumulated depreciation/amortization in the balance sheet and the expense in the P&L are determined.

This article contains the following sections:

Configuring Investments

To configure an accounting rule of the type Investment:

- In the dimension bar, select the combination of data level and reporting entity for which the accounting rule should apply.

- In the tree view, select the desired element (ledger, account, or item).

- Click Edit in the top right to open editing mode.

- If you selected a ledger, open the Balance with carry forward from previous period tab.

- Select Investment as the accounting rule from the Type drop-down list.

- Add or delete a time period to, e.g., configure seasonal differences within a planning period.

Notes on the Add/Delete time period options:

- Newly added time periods are displayed on the Configuration tab.

When deleting a time period, the currently selected tab is always deleted.

Options on the Configuration Tab

The following options are available on the Configuration tab:

Optionally, you can select a VAT/input tax configuration from the drop-down list (see VAT/input tax administration).

The following depreciation/amortization rules are available:

Rule

Description

No depreciation/ amortization

If the investment is not to be depreciated/amortized

Immediate depreciation/ amortization

If the depreciation/amortization is to take effect immediately

Straight-line depreciation/ amortization

If the investment is to be depreciated in equal monthly amounts over its useful life

Declining balance method of depreciation/ amortization:

If the investment is to be depreciated using a fixed annual percentage rate

In the Useful life field, you can enter the term of the depreciation/amortization in months.

This field is only visible if you selected either Straight-line depreciation/amortization or Declining balance method of depreciation/amortization.

In the Percentage field, you can enter the percentage for calculating the annual depreciation/amortization amount.

This field is only visible if you selected Declining balance method of depreciation/amortization.

The following payment types are available:

Payment type

Description

With immediate cash flow impact

If the payment will be received or made within the same month

Time-delayed payment

If the incoming or outgoing payments are made at different times

Down payment transaction

If a down payment is required when the transaction is completed

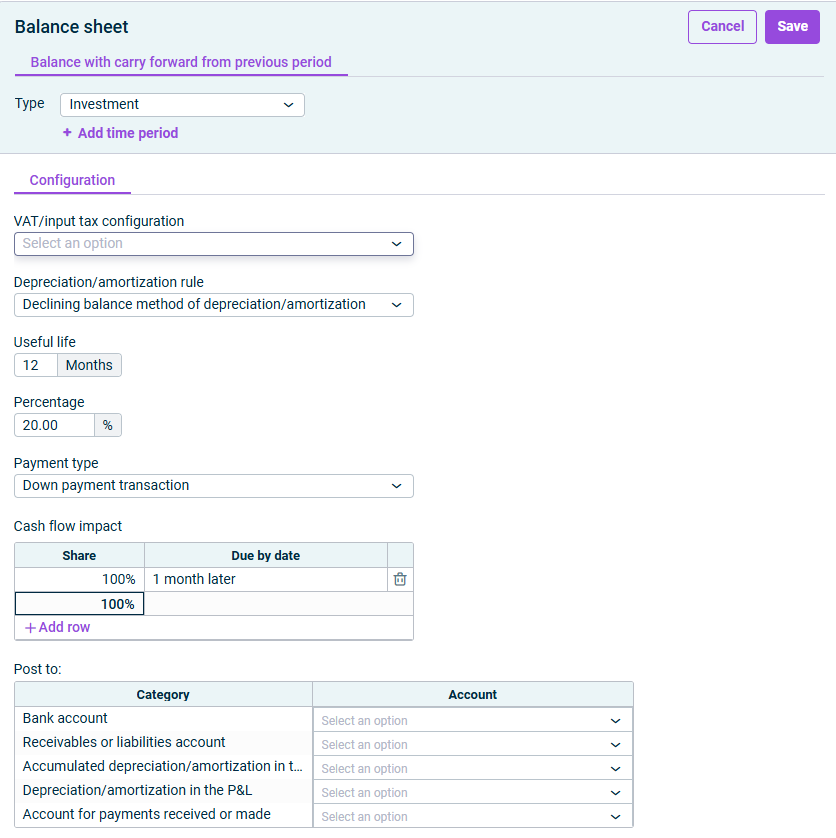

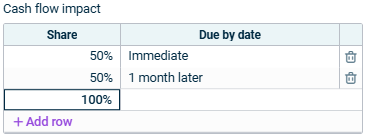

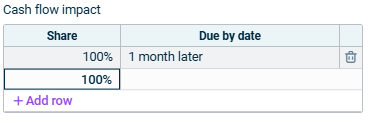

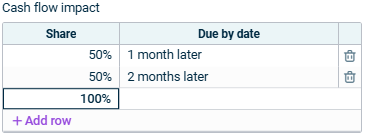

The Cash flow impact section is only visible if you selected Time-delayed payment or Down payment transaction from the payment type drop-down list.

In the Cash flow impact section, specify a due date for the payment, along with percentage of the outstanding receivable or liability to be paid in each case.

Column

Configuration

Due by date

- Enter 0 for immediate payments.

- Enter a positive number for a subsequent payment, e.g. 2 = 2 months later.

- Enter a negative number for an earlier payment, e.g. -2 = 2 months earlier.

To see an example of how average incoming payments can be entered on the Month basis, check Cash Flow Example.

Share

Enter what percentage of the outstanding receivable or liability will be paid by the specified date.

Cash Flow Example

Specify the accounts to which postings will be made in the Post to section.

The accounts to be specified depend on the chosen depreciation/amortization rule and the payment type.

Depreciation/amortization rule

Description

No depreciation/ amortization

- Bank account: An account for the contra entry

- Receivables or liabilities account: An account to which the corresponding value is posted until the cash flow impact takes effect.

(Only with time-delayed payment type)

Immediate, straight-line and declining balance method of depreciation/ amortization

- Bank account: An account for the contra entry

- Receivables or liabilities account: An account to which the corresponding value is posted until the cash flow impact takes effect

(Only with time-delayed payment type) - Accumulated depreciation/amortization in the balance sheet: An account used for correcting the asset value reduced by depreciation

- Depreciation/amortization in the P&L: An account where the depreciation/amortization is to be posted

(Only with time-delayed payment type) - Account for payment received or made: An account to which the down payment will be posted until the service is provided

(Only with down payment transaction payment type)