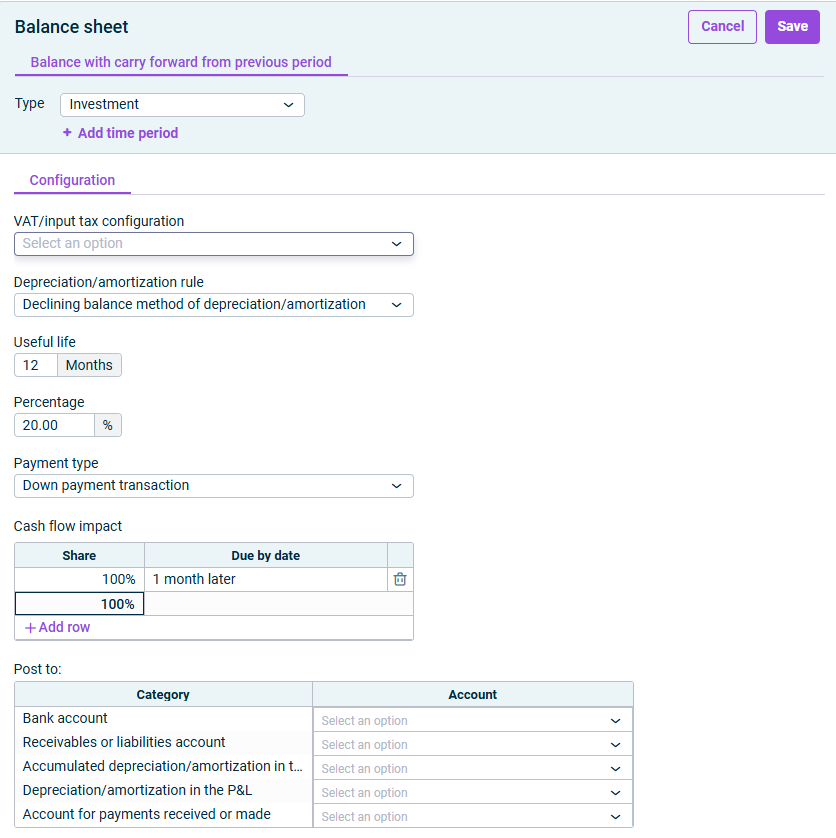

Newly added time periods are displayed on the Configuration When deleting a time period, the currently selected tab is always deleted.

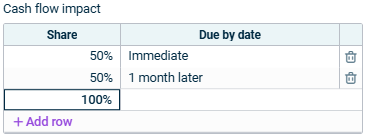

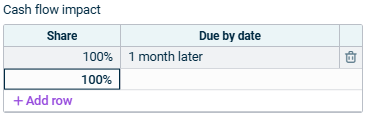

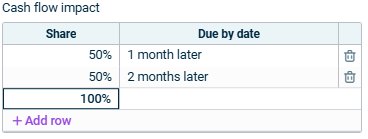

Enter 0 for immediate payments. Enter a positive number for a subsequent payment, e.g. 2 = 2 months later. Enter a negative number for an earlier payment, e.g. -2 = 2 months earlier.

- (Only with | |

- (Only with - - (Only with - (Only with |