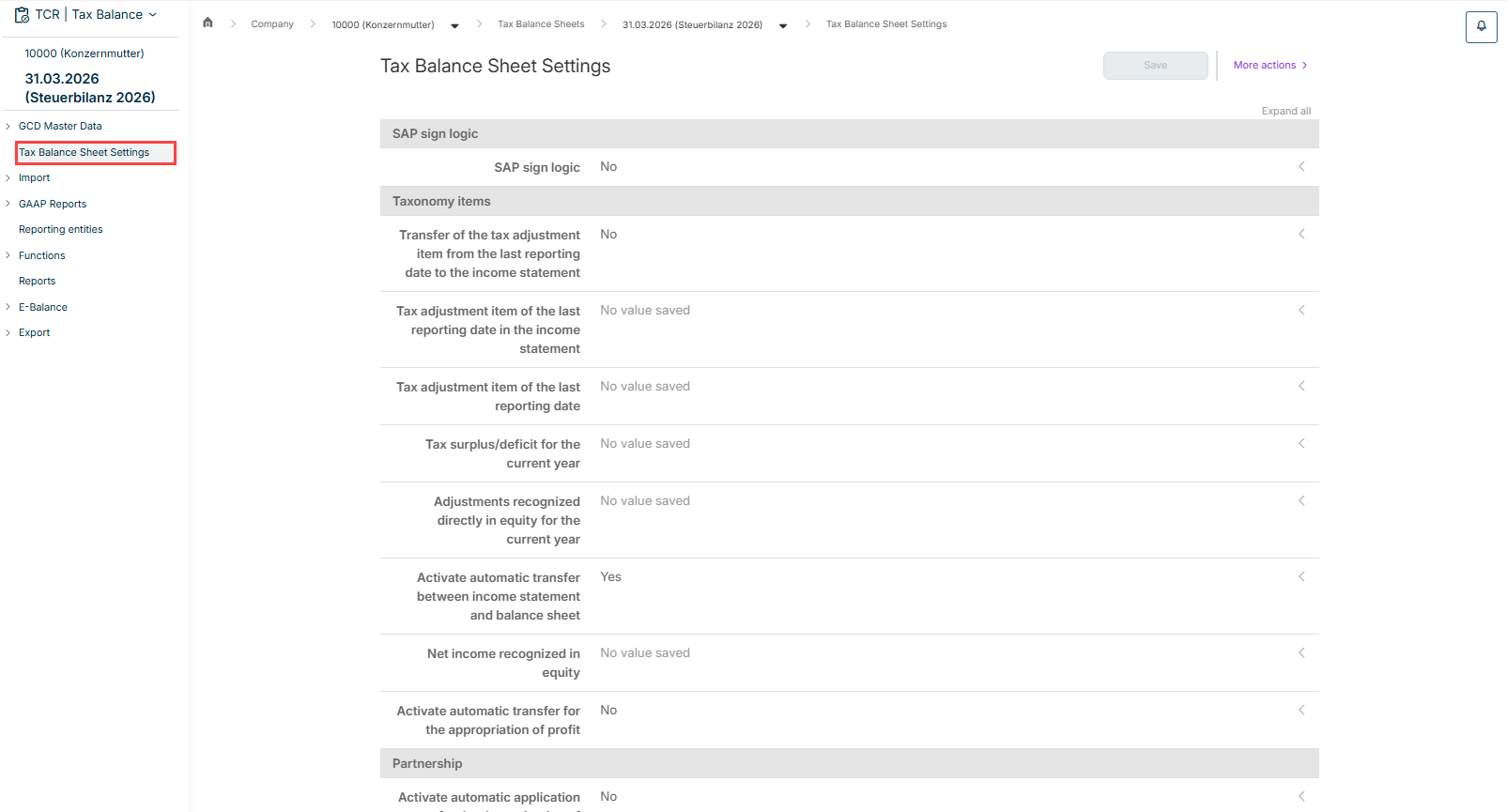

SAP sign logic Taxonomy items The option to activate automatic application for the determination of taxable profit in declaratory procedures Settings for capital account development tax groups mirror image method

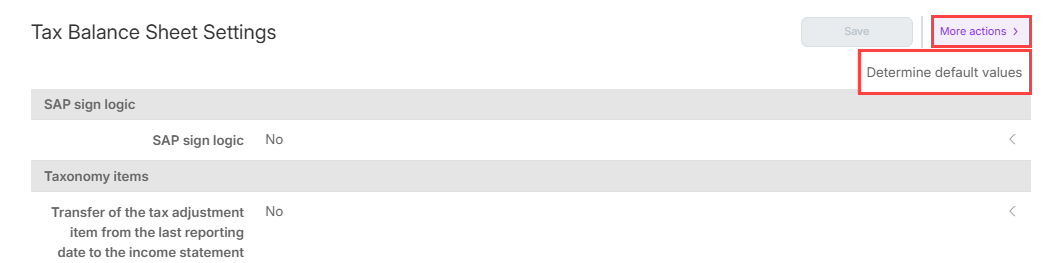

Determine default values Apply from the previous year

Whether the tax adjustment item of the last reporting date is to be included in the P&L of the bank taxonomy Taxonomy items for: Recognizing the balance of the tax adjustment item at the end of the previous year in the income statement of the banking taxonomy The tax adjustment item of the last reporting date in equity The tax surplus/deficit in equity for the current year Adjustments recognized directly in equity in the current year

Whether the net income for the year (or: retained earnings) should be automatically transferred from the income statement (or: appropriation of earnings) to the balance sheet Taxonomy item for the net profit/loss for the year in equity (or in the case of appropriation of profit/loss: net profit/accumulated loss in equity)

If the net profit/accumulated loss rather than the net profit/loss for the year is recognized in equity in the balance sheet, the taxonomy item must be adjusted. In this case, the net profit/loss for the year must not be stored as a taxonomy item, but the taxonomy item retained earnings/accumulated deficit. The taxonomy item net retained profits/accumulated losses corporations commercial partnerships If the net profit/loss for the year from the income statement is automatically transferred to the "Appropriation of profit" section of the report (or to the income statement for insurance taxonomies) as the starting figure for determining the retained earnings/accumulated deficit.

Whether the net profit/loss for the year should be automatically transferred from the income statement determination of taxable profit Whether the taxable profit/loss should be automatically transferred from the determination of taxable profit determination of taxable profit in declaratory procedure

Net income/loss for the year - General partner Net income/loss for the year - Limited partner Tax surplus/deficit - General partner Taxable surplus/deficit - Limited partner

Last updated on May 28, 2026