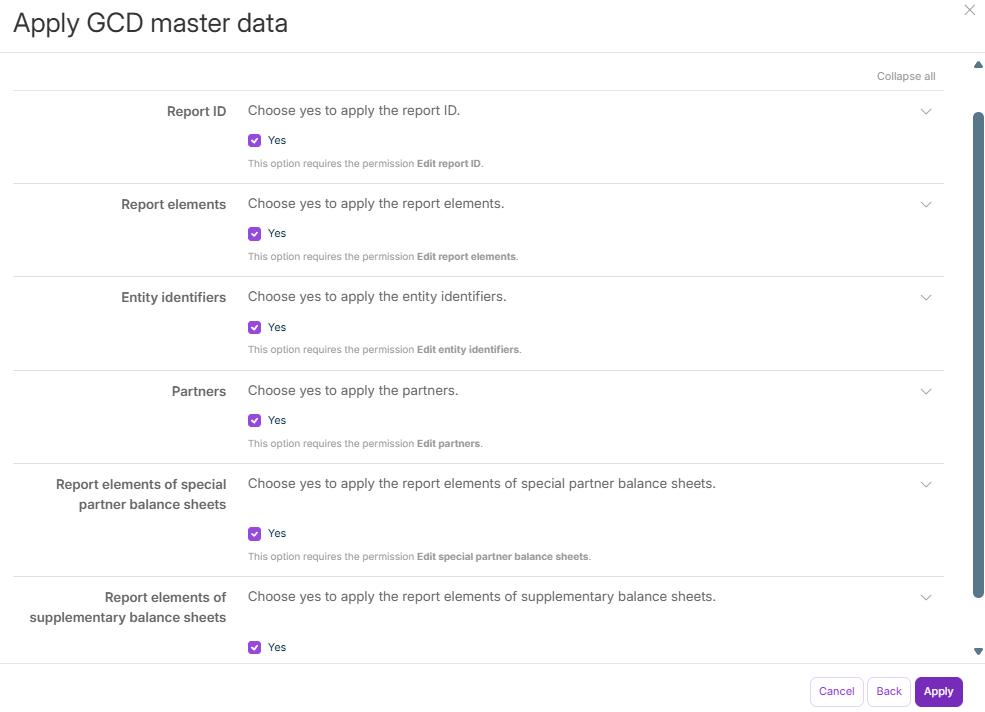

GCD GAAP

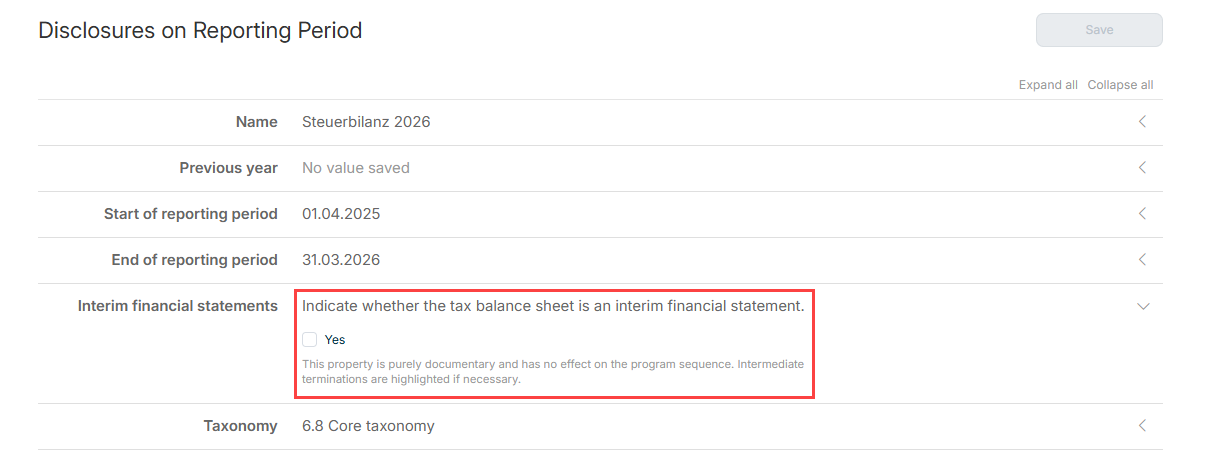

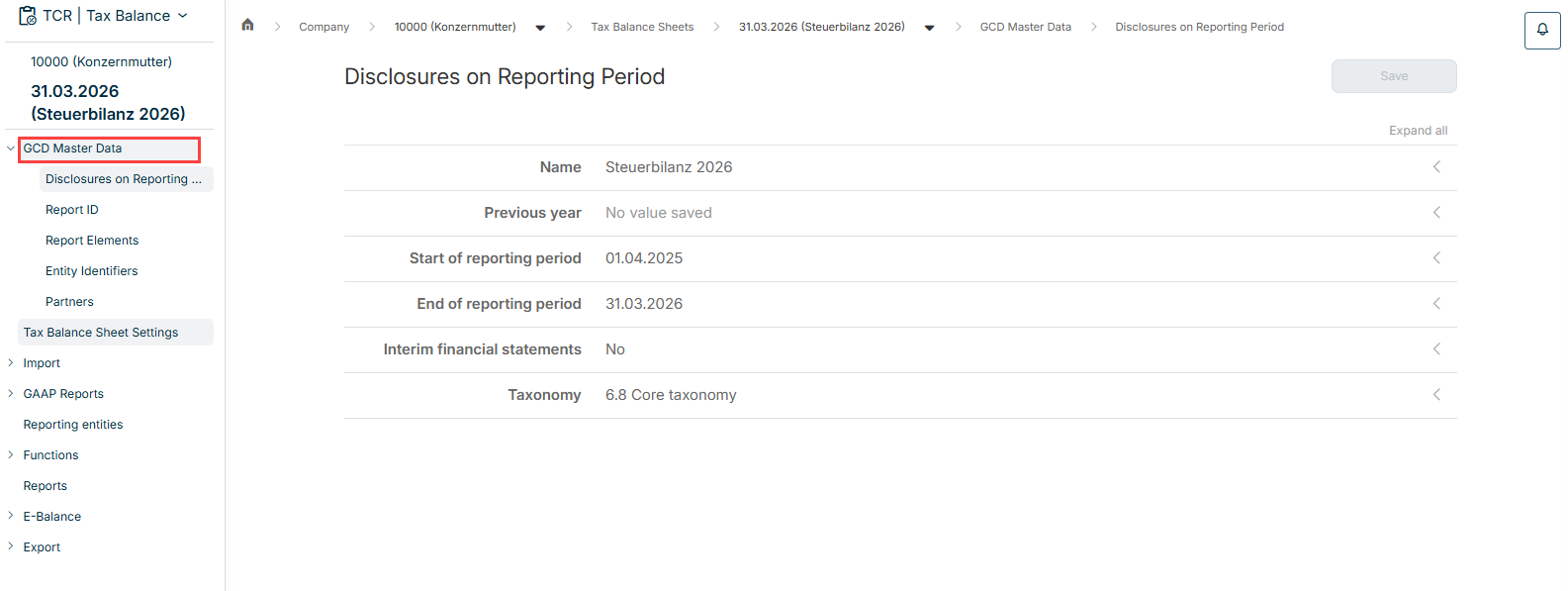

Name Previous year Start of reporting period End of reporting period Indication of whether the tax balance sheet is an interim financial statement Taxonomy Notes on Taxonomies

Annual financial statements Other report

final

For assessment purposes, a report labelled as "final" must be transmitted to the tax authorities.Preliminary

A preliminary report is for information or explanatory purposes only.

First-time Corrected Modified Corrected and modified Same financial statements with more detailed information Otherwise amended

Annual financial statements Reorganization balance sheet, simultaneously annual financial statements Opening balance sheet Interim financial statements Intraperiod figures Reorganization balance sheet Opening balance sheet at begin of liquidation Liquidation interim balance sheet Liquidation closing balance sheet Winding-up accounts (within the meaning of EStG s. 16)

German GAAP German GAAP also meeting tax standards (uniform balance sheet) German tax law

Core taxonomy Accounting regulations for credit institutes, RechKredV - Taxonomy Scheme for Credit Institutions and Financial Services Institutions Accounting regulations for credit institutes, RechZahlV - Taxonomy Scheme for Payment Institutions Accounting regulations for insurances, RechVersV - Taxonomy Scheme for Insurance Companies Accounting regulations for caring institutes, PBV - Supplementary industry taxonomy - here specifically for the area of care facilities Accounting regulations for hospitals, KHBV - Supplementary sector taxonomy - here specifically for the hospitals sector Accounting regulations for owner operated municipal enterprises, Eigenbetriebsverordnung - Supplementary industry taxonomy - here specifically for the area of state-specific ordinances on own-account enterprises Accounting regulations for residential renting businesses, JAbschlWUV - Supplementary industry taxonomy - here specifically for the area of companies covered by the Ordinance on Forms for the Classification of the Annual Financial Statements of Housing Companies Accounting regulations for transport businesses, JAbschlVUV - Supplementary industry taxonomy - here specifically for the area of companies covered by the Ordinance on Forms for the Classification of the Annual Financial Statements of Transport Companies Instructions to BMELV financial statements (forestry and agriculture) - Supplementary industry taxonomy - here specifically for the area of agriculture and forestry

Total cost (nature of expense) method Cost of sales (function of expense) format

Building society (RechKredV) Financial service provider (without settlement services) (RechKredV) German central cooperative central bank (RechKredV) Giro centre (RechKredV) Capital management company (RechKredV) Credit cooperative (RechKredV) Credit cooperative with commodities transactions (RechKredV) Pfandbrief bank (RechKredV) Settlement services (RechKredV) Sparkasse (RechKredV) Universal institute (RechKredV)

Balance sheet Determination of taxable income by comparison of business assets Opening balance sheet without income statement Income statement ends with net retained profits / accumulated loss Income statement Statement of changes in fixed assets (gross) No transmission Carrying amount in financial statements Tax base Carrying amount in financial statements, tax reconciliation and tax base

Register of fixed assets Appropriation of net income Tax reconciliation statement Account balances Determination of taxable income Determination of taxable income in transparent cases Determination of taxable profit for special cases Statement of changes in capital accounts

General information Entity name Legal form Legal form type

Information on consolidated tax group for corporation tax and income tax Tax group type Tax group parent Group share of the tax group parent

Registered office Entity ID numbers Tax number Business tax ID number Federal tax office number

Further information Business Classification of income Option under KStG sec. 1a Entity with determination of income for special cases Transmission option Permanent establishment of foreign company

Affiliation of the shareholderer from to Legal form Natural person - private assets Natural person - business assets Partnership Corporate entity

First and last name